HECM for Purchase is a reverse mortgage that lets homebuyers 62+ buy a home with no required monthly mortgage payments. See how the ANALYZER Pro tool models these loans and demonstrates preserved borrower liquidity.

When most people hear “reverse mortgage,” they immediately think refinance. However, they miss one of the most powerful strategies available to today’s retirees: the HECM for Purchase, often called H4P.

HECM for Purchase allows homeowners age 62 or older to buy a new primary residence using a reverse mortgage, all in a single transaction. Instead of paying all cash or taking on a traditional mortgage with a required monthly principal and interest payment, the borrower brings a sizable down payment and finances the rest through the reverse mortgage.

That structure changes everything. Rather than draining liquidity to buy a home outright, the borrower preserves cash while eliminating the required monthly mortgage payment. For many retirees, that means more flexibility, more security, and better long-term planning.

H4P RULES

The loan amount is based on what’s called the Maximum Claim Amount. This is calculated using the lesser of the purchase price, the appraised value, or the FHA HECM limit for the calendar year. Therefore, if a home appraises below the contract price, the borrower must bring more cash to the loan closing.

Unlike traditional financing, HECM for Purchase also requires a meaningful investment from the borrower. The exact amount depends on factors like age and interest rates, but borrowers should expect to bring a substantial portion of the purchase price.

The home must become the borrower’s principal residence. This product isn’t for second homes or investment properties. In fact, the borrower must occupy the home within 60 days of closing the loan.

ANALYZER EXAMPLE

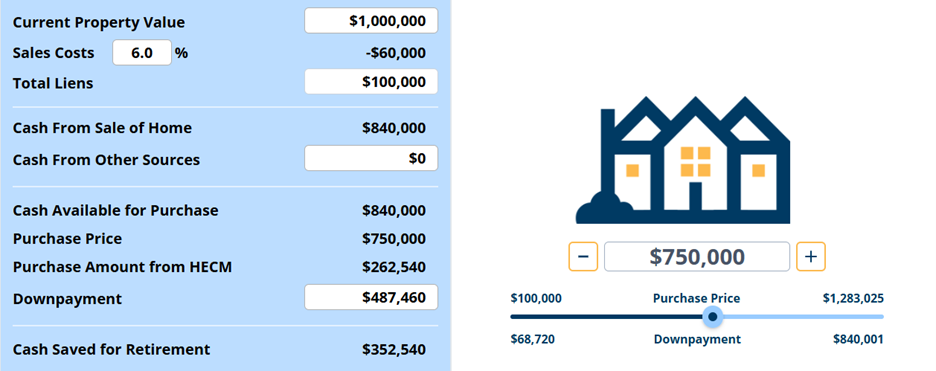

Consider Richard, age 70, who owns a $1 million property and has a $100,000 HELOC to pay off. Let’s use the ANALYZER Pro tool to demonstrate how Richard can downsize and keep more cash for retirement.

On the LEFT side of the screen, we see Richard’s property value, less sales costs, less lien payoffs leaves him with $840.000 in “Cash From Sale of Home.”

By using the slider on the RIGHT, we can see that he could purchase a home with a value of nearly $1.3 million. However, he wishes to downsize to a home valued at $750,000.

Back to the LEFT side, we can see Richard’s downpayment would be $487,460, leaving him with $352,540 in “Cash Saved for Retirement.”

H4P OPENS DOORS

HECM for Purchase allows retirees to relocate closer to family, downsize into something more manageable, or even “right-size” into a home that better fits their lifestyle, without taking on a new monthly mortgage obligation. It’s also a powerful liquidity strategy, helping borrowers avoid tying up all their cash in a single asset.

The bottom line is simple: H4P isn’t just a reverse mortgage attached to a purchase contract. It’s a specialized tool with its own structure, timing, and coordination requirements. But for those who understand it, it offers a smarter way to buy a home in retirement.