A LESA is a portion of reverse mortgage funds reserved to pay taxes and insurance. See how the ANALYZER Pro tool models reverse mortgages with a LESA and how this demonstrates long-term stability and security.

Few reverse mortgage guidelines create more confusion than the Life Expectancy Set-Aside, commonly known as a LESA. Borrowers hear the term and often assume something has gone wrong. Even some originators present it as a deal killer. That framing misses the point entirely. A LESA is not a penalty. It is one of the most important safety features built into the federally insured Home Equity Conversion Mortgage (HECM) program.

Because reverse mortgages do not require monthly payments, it would be impossible to establish a traditional escrow account whereby the lender could pay property charges. Therefore, a LESA is created instead. This is a portion of the borrower’s available funds that is reserved specifically to pay required property charges, typically real estate taxes and homeowner’s insurance.

During the underwriting of the loan file, if there are credit history concerns or if the borrower has residual income that does not meet FHA’s guidelines, a LESA may be required. In simple terms, if the data suggests that keeping up with property charges could become a challenge, the program steps in and builds a solution directly into the loan.

Once established, the LESA is permanent unless the borrower refinances into a new reverse mortgage. And yes, it does reduce the amount of proceeds available upfront. That’s why it can feel disappointing at first glance. But that reaction is based on a misunderstanding.

A LESA is not “lost money.” Rather it is protected borrowing capacity, allocated to cover one of the leading causes of reverse mortgage default: failure to pay property charges. For that reason, a LESA should be encouraged, even if an underwriter does not require one.

The amount of the LESA is calculated using several factors, including the borrower’s annual property charges, life expectancy assumptions, and prevailing interest rates. Importantly, it is not a prediction of how long someone will live. It is an actuarial calculation designed to support long-term sustainability.

ANALYZER EXAMPLE

Consider Sue, age 70, who owns a $600,000 property in Tennessee. Let’s use the ANALYZER Pro tool to demonstrate how a LESA can benefit her over time.

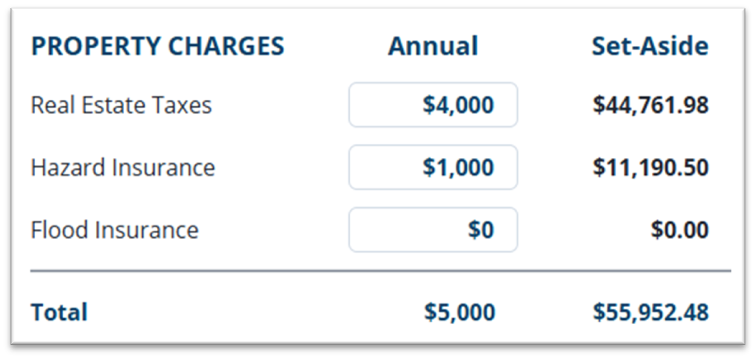

As you can see below, we’ve entered Sue’s annual Real Estate Taxes and Hazard Insurance premiums. ANALYZER will immediately show the exact amount that would be set-aside, in this case $55,952.

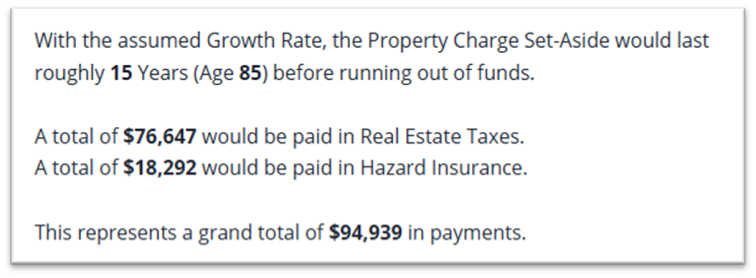

If we assume her property charges increase at an annual rate of 4%, then ANALYZER will show Sue how long the LESA is expected to last and approximately how much would be paid on her behalf over the next 15 years.

Because unused proceeds grow at the same rate as the loan balance, Sue’s LESA of $55,942 is expected to pay nearly $95,000 in property charges on her behalf. That’s $95,000 she won’t need to draw from her retirement savings or other sources.

SELLING A LESA

Ultimately, how a LESA is presented matters. If explained poorly, it sounds like something is being taken away. If explained correctly, it becomes clear that the program is doing exactly what it was designed to do, protect the homeowner’s ability to stay in their home.

A LESA may not be exciting. But it is one of the clearest examples of how reverse mortgage guidelines are built not just to originate loans but to help homeowners age-in-place.